- No posts were found

Mandatory housing insurance, the owners “steal” millions of euros from the citizens

Related Articles

Author: Zylyftar Bregu

The law on mandatory building insurance is violated blatantly, unfairly cumbering citizens with the burden of housing insurance. Only for the houses bought in the period December 2019 – July 2022, the buyers were unfairly “robbed” of 10 million euros, a cost that by law, had to be paid by the builder. On the other hand, the bank does not recognize this insurance policy, and if you apply for a loan, you have to pay another insurance for the building.

About 4 years ago, I.L. signed a preliminary contract with the firm “Arlis Shpk” for the purchase of an apartment in the capital. The company had started the construction of a complex at the intersection of the ring road with Dibra Street.

While he had made the payments according to the contract, when the building was completed and the final contract and mortgage of the property had to be executed, I.L. found himself before a not-so-pleasant surprise. “They told me that I had to pay the building’s ten-year insurance. I resisted, especially when I learned that this insurance policy had to be paid by the builder and was established a year after I had signed the contract. I signed the contract in 2018”, says I.L., preferring not to be fully identified.

However, he was faced with pressure to either pay or the administrator of the “Arlis” company would not sign the final contract.

“Under these circumstances, I paid the contract for the area I bought for ten consecutive years. The bill was about two thousand euros”, – I.L. confesses in disappointment. The administrator of the company refused to comment for “Investigative Network Albania” about this practice of the company, even though initially agreeing to meet us at the company’s premises.

but I.L.’s case is not the only one. Thousands of citizens, who buy apartments since December 2019, are forced to pay the ten-year insurance on the apartment. This policy amounts to 1% of the purchase price, although the law charges this payment to the builders.

One of the newest towers in the city of Tirana, still under construction

More specifically, it is about a decision of November 2019, for the insurance of buildings, according to which, it is specified that:

“The builder/developer/investor delivers to the buyer, simultaneously with the conclusion of the contract for the transfer of ownership of the building, an insurance contract with a term of 10 – (ten) years with the beneficiary buyer/buyers and effective from the date of completion of the works”.

The decision also specifies the formula for calculating the insurance premium so that there are no abuses by the builders.

“The annual insurance premium fee cannot be lower than 0.1% of the insurance amount/liability limit defined in the insurance contract”, the decision states. It charges notaries with responsibility, who must conclude the contract for the transfer of ownership of the building from the investor to the buyer, accompanied by the 10-year insurance contract in favor of the buyer.

“Robbery” through Law

In reality, the complete opposite happens and the “builder’s bill” is charged to the buyer, in flagrant violation of the law. As a result, citizens arbitrarily pay a bill that is not theirs. Statistics show that this insurance package alone captures more than 4 million euros per year, which is “extorted” from the citizen. More than 50% of this insurance package is carried out by an insurance company in the market. Construction and insurance companies, which are largely owned by the same people, have “set up” all the structures.

Most of the notaries, who from being guarantors of the law, have become negotiators for the transfer of this payment, have become part of the mechanism of the builders who “extort” the citizens.

The paradoxical situation is also accepted by the president of the Chamber of Notaries, Mimoza Sadushi.

“Yes, it is true that in some cases the notaries have passed this burden on to the citizens”, Sadushi admits.

Likewise, a dozen institutions that have the task of overseeing the application of this insurance package, namely the Financial Supervision Agency, the Ministry of Justice, the Ministry of Finance and the State Cadastre Agency, have either turned a blind eye or failed to fulfill their duty to implement this law.

“This is an agreement made between the builder and the buyer. If I make some kind of resistance, the builder abandons me and goes to another notary. A single notary does not have the power to fix this problem”, – states notary Erjon Bardhi, who accepts the transfer of payment from the builder to the buyer.

Completely in violation of the law, the practice of transferring this payment is applied in more than 90% of cases.

The Ministry of Justice, after INA Media’s interest and questions on the matter, drafted a long document, without defining the legal form of the document, through which it asks notaries to implement the law.

In the document, the Ministry admits that it has ascertained the fact that the builders pass the building insurance payment to the buyers, in this way breaking the law.

“In this case, we are not before the implementation of the principle of contractual freedom according to Article 660 of the Civil Code, as may be claimed by some notaries. According to this article, the parties really have the right to freely determine the content of the contract, but at the same time they also have the obligation that the content of the contract is within the limits set by the legislation in force”, – writes the Minister of Justice, Ulsi Manja, in the document dated June 16, 2022 with the title, “On the obligation of the notary to implement the legislation in force”.

In the letter, the Minister of Justice emphasizes that the role of the notary in this legal action is not merely formal, but substantial.

But, nearly 3 months after this drawing attention to 420 notaries, the situation has not changed.

From an observation that Investigative Network Albania carried out in several notary offices in Tirana, at the beginning of September 2022, the “guarantors of the law” continue to break it by charging the citizens with the cost of building insurance.

The Ministry of Justice gave an evasive non-answer to the interest of INA Media if notaries have carried out inspections for the implementation of this law.

“Pursuant to the law no. 110/2018 “On the notary”, as amended, the Minister of Justice approves an annual program of inspection of notaries, where each notary office is inspected at regular intervals, but not less than every four years”,

– said the Ministry of Justice, INA Media.

“On the basis of this annual program, the Minister of Justice constantly conducts inspections for notaries throughout the Republic of Albania, for which, in any case, the Minister issues a decision regarding the violations found during the control process. Also, in addition to these inspections, the Minister of Justice also conducts special inspections based on complaints”, concludes the response of the Department of Justice.

But the scandal becomes even bigger. The courage of some notaries goes beyond imagination. Although the citizens are forced to pay the insurance instead of the builder, in the sales contract it is written that this payment is made by the builders. A number of citizens, including I.L., denounce this practice.

“The state can directly take the insurance of the building in the block and not by making a contract for the unit of the building”, – says the notary, Erjon Bardhi.

The Financial Supervision Agency hides the problems it encountered in the practice of applying this insurance premium, behind the article for confidential information.

Skenderbej Square with surrounding towers. Downtown One tower in the distance

“The data, which are made available to the Authority for the activity of the supervised entity, are classified as “Confidential Information” if their dissemination harms the commercial interests or the good name of the entity”. For this reason, we cannot make available to you the copies of the minutes of the monitoring carried out, which are requested by you“, – answered the AMF, to the interest of investigative Network Albania.

Banks “annul” the Government’s decision

Klodjan also paid the building’s ten-year insurance, even though this is the builder’s obligation, and after taking the apartment’s mortgage, he went to one of the second-tier banks for a loan. In the list of documents he had to complete, he confesses that he was quite surprised when he was asked to pay the home insurance for the entire duration of the loan.

“I showed him the insurance that I had paid for, but the bank employee told me that this insurance policy “does not hold up”, Klodjani says. – “I needed that loan, so I reinsured the house, for almost the same amount”.

Paradoxically, none of the second-tier banks, which offer loans, take into consideration the ten-year insurance paid in fulfillment of decision no . 2 0 7, date 22.11.2019 . So, if a buyer wants to get a loan, he has to pay another insurance for the bank.

Spiro Brumbulli, from the Association of Banks explains to Investigative Network Albania that this is because the insurance policy required by the bank has a different object than that of the DCM for the insurance of the building.

“According to the DCM , construction insurance aims to cover building damages related to internal events, mainly the quality of the construction or the development site, but not including damages that occurred directly in the building as a result of fire and earthquake. Meanwhile, the property insurance policy required by the bank has another purpose, which is to insure the property against unexpected external factors and is valid throughout the life of the loan, with the bank as the beneficiary”, explains the Association of Banks.

Sokol Kika, who is one of the investors who paid for the building’s ten-year insurance himself, says that these two policies should be combined. According to him, in the way the scheme currently works, all involved actors are aware that they are forcing a useless product on the market for citizens.

“Each of these actors tries to benefit as much as possible by being part of the process, with the exception of the citizens”, says Kika.

“The state that is the regulator can find a way for the Bank to consider the ten-year insurance policy between the builder and the buyer”, – further explains the builder Sokol Kika.

Nentitull: Millions of euros from the insurance policy

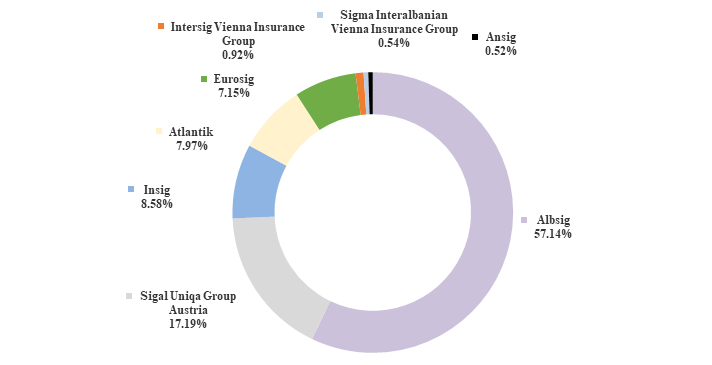

In the first year of applying this insurance premium (2020), according to the Financial Supervision Agency, insurance companies have collected more than four million euros.

Fig. 1. Year 2020 – Market sharing – Construction Liability Insurance

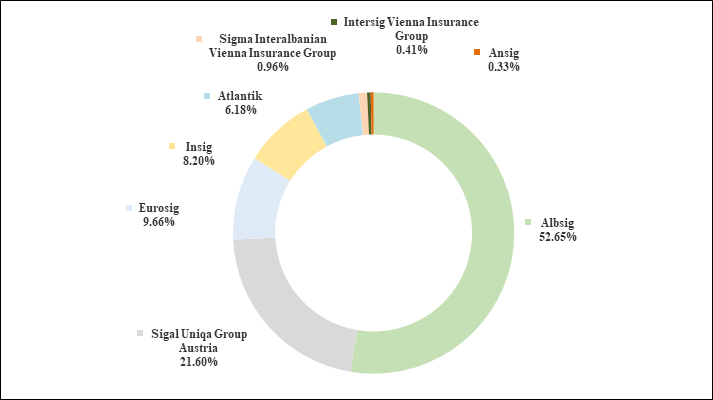

In the second year, more than 5 million euros were collected.

Fig. 1. Year 2021 – Market sharing – Construction Liability Insurance

While in the first seven months of 2022, around 1.3 million euros have been collected.

Fig. 3. Year 2022 – Market sharing – Construction Liability Insurance

According to the official website of the AMF, the majority of the constructions’ insurance policies were provided by the Albsig company, with over 55% of the market. After that there are two other companies, Atlantik and Sigal Uniqa Group Austria, with approximately the same percentage, respectively 15% and 14%. The other six companies have a negligible market in this insurance premium. In 2021, Albsig again maintains the dominant position in construction liability insurance, with around 60%, and also in the first 7 months of 2022.

The insurance company Albsig did not answer questions related to the strategy used by it to ensure the dominant majority of the market in this type of insurance. While its rival companies, which have not participated in the “sharing of the pie” of this type of insurance, are reluctant to speak publicly. But, confidentially, they show some of the maneuvers that are done in the market of this insurance.

“Despite the fact that the decision forces the insurance premium to be no less than 1% of the sale price, the market offer becomes 50, 60 and sometimes even 80% lower. This offer is “hidden” behind the concept of mediation commissions. So, if an insurance premium costs one thousand euros, the company pays only 500 euros, or in the best case, 200 euros”, explains the sales agent of an insurance company who wishes to speak on condition of anonymity.

The second problem is related to the fact that none of the insurance companies in Albania re-insure this insurance portfolio.

“Albania is known as a seismic zone and one of the risks that is covered under this product is the earthquake, which makes it a product with high exposure. The domestic market lacks the capacity to handle this type of damage on its own, and reinsurance for this portfolio is necessary, even in powerful re-insurers abroad, with technical experience and high solvency”, – it is written in a document that an insurance company in the market has written to the Financial Supervision Agency.

From confidential sources, it is known that almost all companies that offer this insurance policy have tried to “shift” the responsibility of reimbursement by re-insuring powerful partners abroad.

Faced with numerous problems with constructions in the country, large international companies have rejected the offer of Albanian companies.

According to them, the problem starts with the quality of the constructions and an institution independent from the state is needed to supervise the construction of the building from the foundations to its end.

“First, how can we insure a building from construction problems, when we don’t have an independent institution to certify the construction?”, – say the representatives of the insurance companies.

The second impasse is related to the fact that the Decision of the Council of Ministers or the AMF has not established a liability limit (i.e. the maximum amount that is taken in insurance).

“Such practices, when the promise to cover damages is unlimited, are not applied by international companies”, they say further.

The third impasse is related to deficiencies in terms of insurance, providing coverage for individual units and not for the building as a whole.

“What happens if common environments are damaged? Who is responsible for them? But if there are still unsold apartments in a building? How can partial reconstruction be done?”, – the insurers raise concern.

As long as Albanian companies or institutions do not have clear answers to these issues, none of them has found a partner to carry out the re-insurance of this policy.

Building insurance, useful only for insurance companies

Decision number 650, dated 02.10.2019 “On Construction Insurance”, aims to establish a mechanism for covering damages to buildings that are damaged due to soil problems or construction deficiencies and the risk of collapse is obvious, whether partial or complete.

The powerful earthquakes that damaged hundreds of buildings in Albania, in the fall of 2019, served as a reason for the government, five years after the adoption of the law “On planning and development of the territory” to approve the mandatory insurance. The law passed in 2014 is a bad translation of the Italian law governing building insurance by the builder.

In Albania, the content of this insurance policy is described by experts in the field as having many structural deficiencies, unclear in implementation and above all as a policy that will never be used for reimbursement.

“Even if the whole of Tirana is flattened, the insurance companies can avoid the reimbursement of this policy, because it will have to be proven that the destruction came as a result of deficiencies in the construction. Practically impossible”, says the deputy director of an insurance company on condition of anonymity.

In the government’s decision on building insurance, it is clearly sanctioned that the builder/developer/investor delivers to the buyer, simultaneously with the conclusion of the contract for the transfer of ownership of the building, an insurance contract with a term of 10 years, with the buyer as the beneficiary and with effect from the date of completion of works.

20 days after this decision, the Financial Supervision Authority approved the elements and general conditions of the compulsory construction insurance contract, with decision no . 207 , dated 22.11.2019 .

“The insurance company is obliged to compensate the insured/beneficiary for damages that occurred directly in the building, such as: Total or partial collapse of the building; the building clearly poses a risk of collapse; or other serious defects; which occur as a result of problems related to the defects of the land on which the construction was carried out or due to one or several construction defects”, – it is stated in article 5 of this decision, which defines the three cases when the builder can compensate the buyer of the apartment. .

The time of only 20 days during which the decision on the elements and conditions of the contract was drawn up and approved shows that the process was rushed.

“The Financial Supervision Agency, even though it sent us a letter through which it sought our opinion and proposals, did not reflect any of the ideas of the insurance companies”, – says the deputy director of the insurance company, who wishes to speak on condition of anonymity.

The rush to draw up this insurance portfolio has been accompanied by problems since the first days of application. Even to this day, experts are unclear when this government decision, approved in November 2019, “extends” its legal power.

Experts explain that it was unclear whether the insurance policy was necessary for all first-time sales deeds from the builder to the buyer, after the entry into force of the government decision, November 2019; only for sales contracts for construction units that have received a certificate of use after the entry into force of law no. 107/2014 (the law from which the decision on mandatory building insurance originates), or only for sales of construction units that have received certificate of use after the entry into force of the government decision in November 2019.

“A builder who received a construction permit in 2017, but completed the building in 2020 and will sell the apartments in January 2020, should he insure the building or not”, – asks the president of the Chamber of Notaries, Mimoza Sadushi, unclear about the answer, even after two years of having this concern.

The second problem was related to the fact that this insurance contract would include only the sale or even the deed of donation or the portion that benefits the owners of the land in multi-storied buildings.

From a written communication between the Cadastre Agency and the Ministry of Finance or the Ministry of Infrastructure, whose documents are at INA’s disposal, it is clear that each of the regional cadastre agencies has given the solution they saw as the most appropriate to the above problems.

The created chaos is accepted through a long communication through documents, between the Head of the Cadastre Agency Artan Lame and the Ministry of Energy and Infrastructure. Due to the delay in the response and its ambiguity, when it was given, the head of the Cadastre Agency, Artan Lame, proposed the modification of the government’s decision.

But the Prime Minister did not agree. “Ina Media” has seen an exchange of letters from the head of the Cadastre, Artan Lame, according to which he excuses himself for having his hands tied by the government that does not accept the correction of the land registry. Referred to letter no. 1435/1, dated 14.07.2020, the Council of Ministers has indicated to the Cadastre that since the proposal of this decision was made by the Ministry of Finance and Economy as well as the Ministry of Energy and Infrastructure, the right to propose changes belongs only to these two structures.

“I am convinced that I have fulfilled my obligations, but the builder, the state together with my notary “stole” the money that I barely secured”, – insists I.L., aware that he cannot do anything to have justice.

This article is published by “Investigative Network Albania”

{kind=link}

Let me tell You a sad story ! There are no comments yet, but You can be first one to comment this article.

Write a comment